Japan’s railways are the finest in the world. Other countries can copy its formula.

Japan is the land of the train. 28 percent of passenger kilometers in Japan are travelled by rail, more than anywhere else in the developed world. France achieves 10 percent, Germany 6.4 percent, and the United States just 0.25 percent. Travel in Japan is over a hundred times more likely to be by rail than travel in the United States.

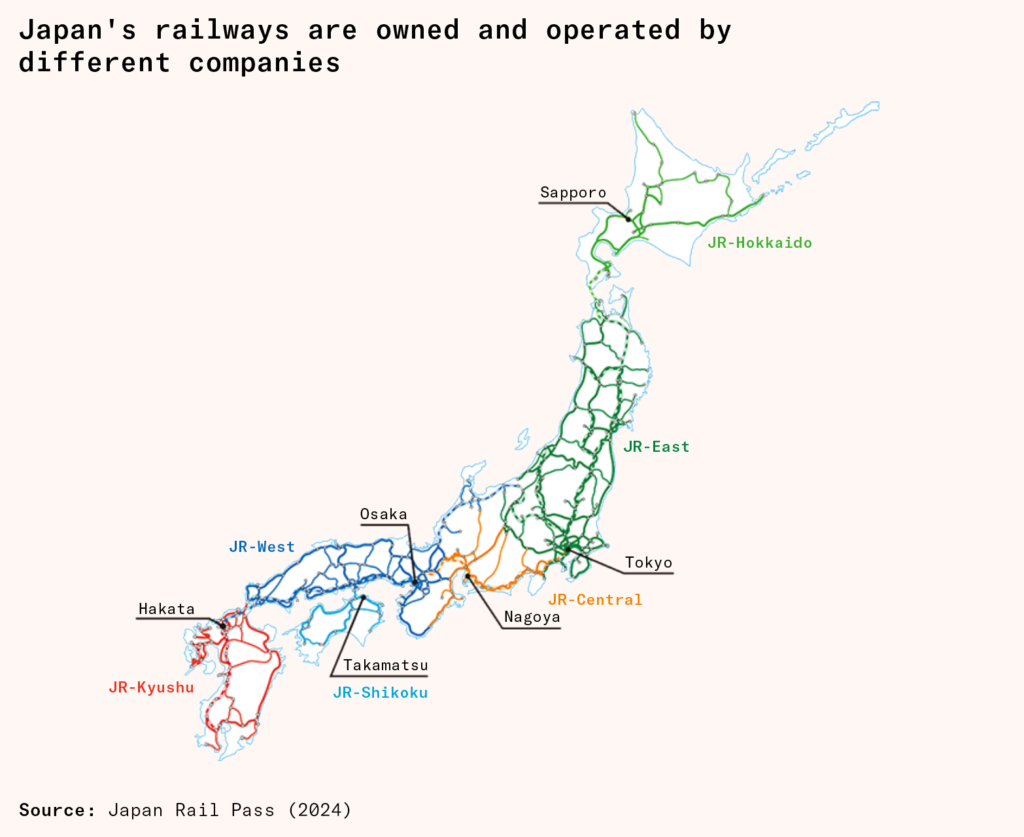

Japan’s vast railway network is divided between dozens of companies, nearly all of them private. The largest of these, JR East, carries more passengers than China’s entire railway system. Each year, JR East carries four times as many passengers as the whole British railway system, even though it has fewer kilometers of track, serves about ten million fewer people, and competes with eight other companies. Japan’s railway system turns a large operating profit and receives far less public subsidy than European and American railways.

Subscribe for $100 to receive six beautiful issues per year.

In most developed countries, the railways have struggled since the rise of the automobile in the 1950s. From this point on, North America saw the near-total replacement of passenger trains with cars and planes. In Europe, it meant vast government financial support to keep the lines open.

Japan’s different trajectory is often attributed to culture: the Japanese are conformists who are content to take public transport, unlike freedom-loving Americans who prefer to drive everywhere. Europeans are somewhere in between. Culture is also used to explain the incredible punctuality of Japanese railways.

These cultural explanations are wrong. The Japanese love cars, but they take trains because they have the best railway system in the world. And their system excels because of good public policy: business structure, land use rules, driving rules, superior models for privatization, and sound regulation have given Japan its outstanding railways.

This is good news for friends of rail. Culture is built over centuries, and replicating it is hard. But successful public policies can be emulated by one good government. Much about Japan’s railway system could be replicable around the world.

Japan’s railway companies

Today, the most striking institutional feature of Japanese rail is that it is privately owned by a throng of competing companies.

The railway arrived in Japan in 1872, during the Meiji Restoration, which opened the country up to foreign trade, ideas, and technologies. Like most Western countries, Japan nationalized its railways in the early twentieth century, creating what became known as Japanese National Railways (JNR). But it did not nationalize all of the lines, focusing only on mainline railways of national importance, and new private railways were still permitted.

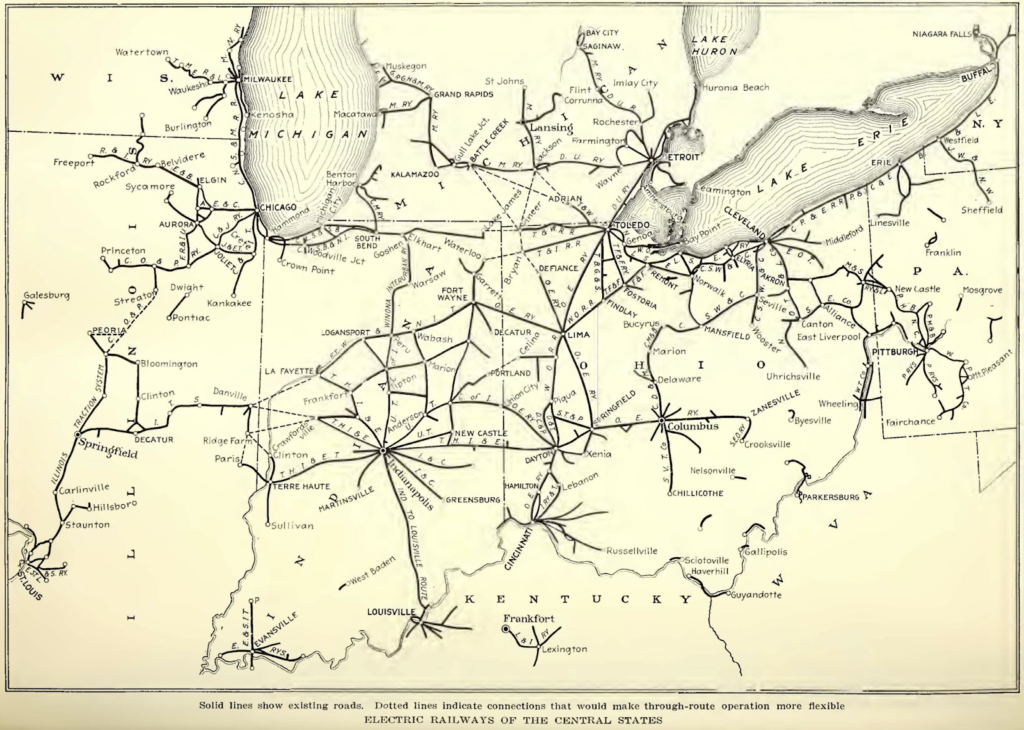

Between 1907 and World War II, Japan saw a boom in new private electric railways, coinciding with rapid urbanization. Technologically, most of these private railways were similar to the famous interurbans in the United States: they were basically electric trams, but running between cities as well as within them. The American network eventually withered, and almost nothing of it survives today. In Japan, however, the network consolidated, and the light tramlines gradually evolved into heavy-rail intercity connections.

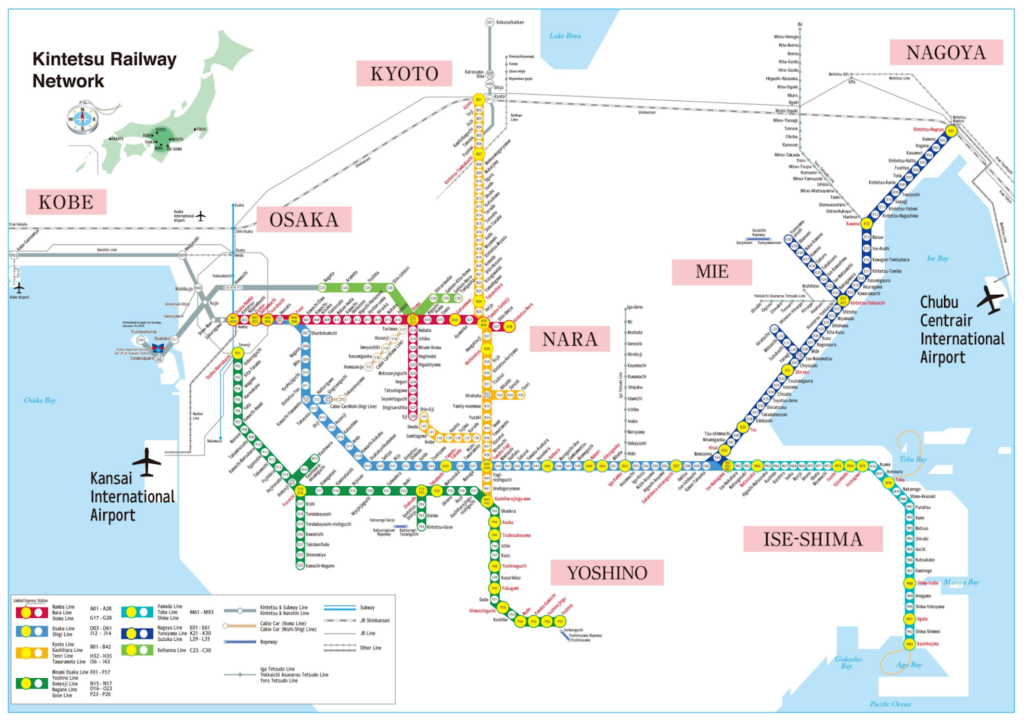

These companies are today known as ‘legacy private railways’ on account of their having been private since their inception. There are eight legacy private railways in the Tokyo metropolitan area, five in the Osaka–Kobe–Kyoto megalopolis, two in Nagoya, and one in the fourth city of Fukuoka. There are also dozens of smaller ones elsewhere. In the three largest urban areas, these operators account for nearly half of railway track and stations, as well as a plurality of ridership. The largest, Kintetsu, not only operates urban services, but a whole intercity network stretching from Osaka to Nagoya.

These companies often compete head-to-head. At its most extreme, three separate commuter lines compete for the traffic between Osaka and the port city of Kobe, running in parallel, sometimes fewer than 500 meters apart.

Meanwhile, the nationalized railways were managed by JNR. In the postwar era, JNR was responsible for building the famous Shinkansen system, as well as running commuter and long-distance lines throughout Japan. But in 1988, it was largely privatized, broken into six regional monopolies for passenger services together with a single national freight operator. These are collectively known as the Japan Railways Group (JR).

This means that Japan has ended up with six railway companies that trace their descent to the nationalized railways, the sixteen big legacy companies that have always been private, and a host of minor legacy railways, as well as numerous underground metros (some private, some municipally owned), monorails, and tram systems. This institutional diversity is striking enough. But equally striking is the consistent business model that has evolved amidst this pluralism: the railway that builds a city.

Railway-led urbanism

If I take a train to go for a solitary walk in the countryside, the railway company can capture some of the value it creates by charging me for the journey, just as other companies capture the value of the goods and services they provide by charging for them. However, if I take a train to visit family, clients, a theater, or a shop, an important difference appears. The railway can capture the value it creates for me by charging me a fare, but it cannot capture the value it creates for those at my destination. As transport infrastructure creates benefits that produce no revenue for providers, free markets rarely build enough of it.

Japan has partly solved this problem by enabling railway companies to do a great deal beside running railways. Take the example of the Tokyu corporation, one of the legacy private railways in southern Tokyo. You can not only travel on its trains, but also ride a Tokyu bus, live in a Tokyu-built house, work in a Tokyu office complex, see a doctor in a Tokyu hospital, buy groceries in a Tokyu supermarket, spend an afternoon at a Tokyu museum-theater-cinema complex, take your children to their amusement park, and even die in a Tokyu retirement home. The positive spillover effects of the railway on these things are captured by Tokyu because it owns them. The president of Tokyu has said:

I think that though we are a railway company, we consider ourselves a city-shaping company. In Europe for instance, railway companies simply connect cities through their terminals. That is a pretty normal way of operating in this industry, whereas what we do is completely different: we create cities and then, as a utility facility, we add the stations and the railways to connect them one with another.

This model was pioneered in the 1950s by what became Hankyu Railways. Hankyu’s network connects central Osaka to its northern suburbs, as well as Kyoto and Kobe. Its innovative founder Kobayashi Ichizo first built suburban housing, then a department store at the terminal station; he then created a hot spring resort, a zoo, and his own distinctive brand of all-women musical theater, the Takarazuka Revue. He also began to run bus services to and from his stations. Other companies emulated Hankyu’s example: Tokyo Disneyland is a collaboration between Disney and the Keisei Railway, while Hanshin in Osaka owns the Hanshin Tigers baseball team.

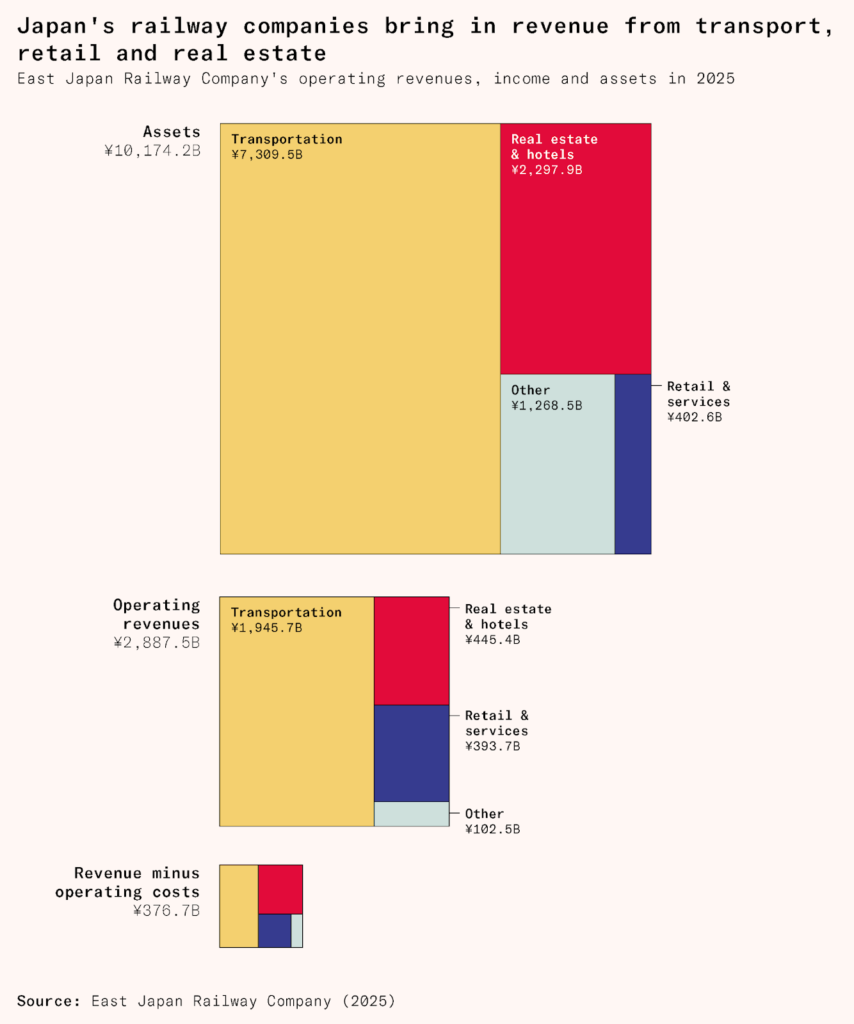

Core rail operations are profitable for every Japanese private railway company, but they usually only account for a plurality or a small majority of revenue. The rest is contributed by their portfolio of side businesses. There is a natural financial synergy between the reliable but unremarkable cash flow of train fares and the profitable but riskier real estate and commercial side of the business. Railway companies’ side businesses also attract people to live and work on their rail corridor, reinforcing the customer base for the railway services themselves.

This virtuous circle is enabled by transit-oriented development. Japan’s liberal land use regulation makes it straightforward to build new neighborhoods next to railway lines, giving commuters easy access to city centers. It also enables the densification of these centers, which means that commuters have more places they want to go.

Railways cost a lot to build, but once they are built, they can move enormous numbers of people, far more than a road of similar size. This means that they work best in cities with a high density of people, jobs, and other activities. In 2019, New York City was the only American city where rail had a higher modal share than cars, in part because Manhattan has 2.5 million jobs, two million residents, and 50 million tourist visits crammed into 59 square kilometers.

This does not mean that rail-oriented cities must be structured like Chinese cities: islands of high-rise apartments connected by metros and separated by motorways. Japanese cities have the lowest residential density in Asia, and a plurality of the Japanese live in houses, usually detached ones. The urban area of Tokyo, the densest Japanese city, has a weighted population density less than that of many European cities, including Paris, Madrid, or Athens. Japanese cities have vast low-rise, predominantly residential suburbs, built at densities that might be higher than what is typical in the United States, but that would be quite normal in Northern Europe.

What makes Japan’s cities particularly suited to rail is thus not their residential districts, but their huge and hyperdense centers. These really are special: the cores of Tokyo or Osaka are unlike anything that exists in Europe or North America. Many of their features are famous worldwide: the vertical street zakkyo buildings, underground streets, shopping streets under rail tracks, covered arcades, elevated station squares, and vertical cities. Getting millions of commuters and shoppers into these downtowns is where rail excels because its extreme spatial efficiency means that infrastructure with a relatively modest footprint can transport vast numbers of people into a small area.

None of this emerged from a coherent masterplan of transit-oriented development like Copenhagen’s Finger Plan or Curitiba’s Trinary System. Postwar Japanese opinion was committed to decentralization both to rural peripheries and to the suburbs through greenbelts, motorways, and new towns.

Instead, this variety and adaptability around railways is possible because of the way Japanese urban planning works. Since 1919, Japan has had a standardized national zoning system, but it is much more liberal than development control systems in Western countries. The Japanese authorities did not intend or even desire dense urban centers, but they did not prevent them, rather like nineteenth-century governments in the West.

This liberal zoning system is reinforced by private access to city planning powers. Thirty percent of Japan’s urban land has been subject to land readjustment, where agreement among two thirds of residents and landowners in an area is enough to allow its replanning, including compulsorily taking and demolishing land for amenities and infrastructure. Initially land readjustment was used only to assemble rural land for urbanization, but over time it was increasingly used to redevelop already urbanized areas, and new variants were created to build the skyscrapers that surround the major stations of central Tokyo.

The history of the private railway companies could be written as a story of land readjustment projects: the initial building of the lines in the interwar years proceeded through one land readjustment project after another. Postwar improvements such as double-tracking, platform lengthening, and constant redevelopment of stations and their immediate thresholds were only possible because the railways could secure land takings cooperatively with local businesses and landowners.

Perhaps the greatest example of this phenomenon involved Tokyu. In 1953 the company decided to build the Den’en Toshi Line, or Garden City Line, to serve a rural area southwest of Tokyo. This would be enabled by a series of land readjustment projects collectively among the largest in Japanese history.

Over 30 years, 3,100 hectares were covered, of which only 36 percent was devoted to residential and commercial development, with 20 percent for forest and parks, 17 percent for roads, and much of the rest for watercourses. The population of the land readjustment zone would rise from 42,000 in 1954 to over 500,000 in 2003.

By connecting the affluent southwestern suburbs to Tokyu’s main real estate hub next to Shibuya station, now the second busiest in the world, the Den’en Toshi Line allowed Tokyu to become the largest private railway by revenue and ridership. The Japanese government and academics generally consider the Den’en Toshi Line to be the best corridor of transit–oriented development in Japan.

But the railway-as-city-builder model is not the only reason Japanese railways have been able to thrive. European countries usually prohibited railways from running real estate side businesses, but in the United States and Canada the practice was extremely widespread in the nineteenth and early twentieth centuries, and many famous railway suburbs were developed this way. Despite this, passenger rail in these countries collapsed in the mid-twentieth century. Part of the difference was that Japan did not extend the same implicit subsidies to cars as Western governments did.

Pricing driving

The land of Toyota, Nissan, and Honda is not an anti-car nirvana. In fact, Japan has excellent motorways, and across the country as a whole a small majority of journeys are made by car. But Japan is a place where cars and car-oriented lifestyles compete on a level playing field.

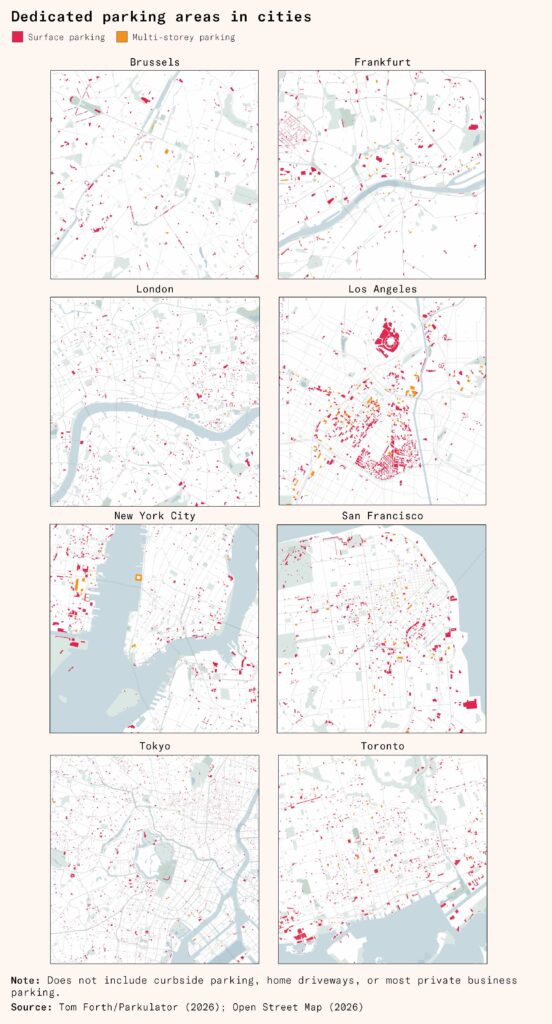

Japan is one of the only countries to have privatized parking. In Europe and North America, vast quantities of parking space is socialized: municipalities own the streets and allow people to park on them at low or zero cost. Initially with the intention of encouraging the provision of more parking spaces, Japan made it illegal to park on public roads or pavements without special permission. Before someone buys a car, they must prove that they have a reserved night-time space on private land, either owned or leased.

Since parking on public land is banned, municipalities are not worried about overspill parking from developments with inadequate private parking. They therefore have no reason to impose parking minimums on developments: the market is left to decide whether parking is the most valuable use of private land. Where land is abundant, as in rural areas, suburbs, or small towns, private parking is plentiful. But in city centers, it is outcompeted by other land uses. According to the late Donald Shoup, central Tokyo has 23 parking spaces per hectare and 0.04 parking spaces per job, compared with 263 and 0.52 for Los Angeles. Even Manhattan, the densest urban area in North America with the lowest levels of car ownership, has about 60 parking spaces per hectare.

Japanese roads are expected to be self-financing. Motorways are run by self-contained public cooperatives, very similar to the statutory authorities that ran English roads and canals between 1660 and the late 1800s, and funded by tolls on their users. Vehicle registration taxes, which are allocated to localities for road construction and maintenance, are worth three percent of the Japanese government budget.

These measures, adopted in the 1950s, were not intended to suppress car use – the point was to fund a massive road expansion – but they have forced private vehicles to internalize many of their hidden costs. In the Tokyo urban area, the average household spends 71,000 yen ($450) each year on public transport fares and 210,000 yen ($1,350) on car purchase and maintenance costs.

But the private car was not the only competitor faced by the private railways. For eight decades in the twentieth century, they also had to face the juggernaut of Japanese National Railways. Its privatization in 1988 removed the final obstacle to creating the world’s best railway system.

Privatization

Railway privatization in Britain, New Zealand, Argentina, and Sweden has had a mixed reception, and all of those countries, apart from Sweden, have taken steps to reverse it. In Japan, it has been so successful that the government subsequently privatized the metro systems in Tokyo and Osaka.

In the postwar period, JNR enjoyed real successes. It built the revolutionary Shinkansen, the first high-speed railway in the world. It also aggressively electrified and double-tracked major trunk lines, quadruple-tracked lines into and out of major cities, and added city-center loops and freight bypasses. But these achievements were overshadowed by two problems.

The first was politics. Many countries adapted to the rise of the car by closing the least profitable parts of their passenger rail network, like the consolidation of American freight rail into the Class I operators or the Beeching Axe in Britain. In Japan, however, the ruling Liberal Democratic Party drew its support from rural constituencies, whose support it retained with pork–barrel politics. Its ‘rail tribe’ group, led by rural MPs, prevented JNR from adapting itself to mass motorization.

JNR therefore did not amputate gangrenous rural and freight services that imposed heavy costs with few benefits. Worse, it continued to build new loss-making rural railway lines, known in Japanese as Gaden-intetsu, or railways pulled into the rice field.

The second problem was organized labor. In general, Japanese trade unions are known for their moderation and responsibility, a generalisation that also held true for the unions at the legacy private railways. The JNR unions, however, became highly militant, secure in the knowledge that their nationalized employers could never go bankrupt. Their largest series of strikes in 1973 provoked riots from commuters.

The railway unions imposed overstaffing on revenue-generating urban services, at a time when both international and private domestic operators were reducing staffing requirements against a backdrop of higher wages and the growing automation of signaling and ticketing. As a result, 78 percent of JNR’s costs were related to labor, compared to 40 percent for other Japanese railways. The average worker at a private railway was 121 percent more productive than their JNR counterpart.

By the early 1980s, only seven out of 200 JNR lines made a profit. Successive governments deferred serious reform, running up debt, cutting down investments in new urban lines, raising ticket prices to twice those of comparable private railways, and increasing subsidies – which rose until annual subsidies equaled the total cost of the Shinkansen.

In 1982, Prime Minister Yasuhiro Nakasone started to privatize the railways. Unlike other countries, Japan simply returned to the traditional private railway model of the nineteenth and early twentieth centuries: tracks, trains, stations, and yards were owned by vertically integrated regional conglomerates.

There are substantial advantages to vertical integration. Railways are a closed system that has to be planned as a single unit. Changing the timetable at station A can affect the timetable at station Z; buying new trains that can travel faster might require changes to the infrastructure so they can reach their top speed, which in turn requires rewriting the timetables. This becomes especially complicated if different services share tracks. To prevent delays from propagating from one service to another, the timetable needs to be carefully designed to make best use of the available infrastructure.

The starkest effect of privatization was a massive and immediate increase in labor productivity and profitability relative to the legacy private railways. In fact, this began before privatization: its mere threat strengthened the government’s hand when bargaining with the unions and forced JNR to begin closing rural lines.

Privatization saw a general trend of productivity improvements, following a big one-time improvement between 1982 and 1990, when the workforce was cut by more than half, 83 loss-making lines were removed, and JNR’s debts were transferred to a holding company.

The second great advantage of privatization was to allow the JR companies to emulate the railway-as-city-builder model of the legacy private railways: for instance, JR East owns two shopping center brands, a ski resort, a coffee chain, and even a vending machine drink company. The JR companies have not ignored their rail business: they have continued to build new high-speed lines and urban tunnels, upgrade stations, and implement a host of other improvements such as the introduction in the 1990s of smart cards that allow passengers to pay their fare with a tap.

Regulation

This does not mean that the Japanese railway industry is a pure creature of free enterprise. No railway system ever has been. The Japanese system has found an equilibrium that makes rail policy explicit and limited. Leaving aside railway safety and business regulation, there are two main policy levers: fare maximums and capital expansion subsidies.

Price controls are often cited as a classic example of misguided government intervention, whether through rent controls, caps on the price of gasoline, wage freezes, or minimum agricultural prices. Tokyo’s infamously crammed trains are a symptom of underpriced rush hour traffic.

Railways have market power because the substitutes for railway trips – coaches, cars and planes – are quite a different product. This monopolistic position has historically meant trouble: monopoly systems, whether private or public, have a tendency to abuse their position to charge higher prices and run bad services. For this reason, the private monopolies that were common in the Western world before World War I often had price controls imposed on them. For example, most of the American streetcar networks were operated as long-term, price-controlled franchises granted by the city.

Price maximums, if set too low, could have ruined Japan’s railways. This is exactly what happened to many Western transit services after the First World War. But the postwar Japanese practice has capped fares generously. The system is explicitly designed to maintain profitability per rider, which in turn incentivizes the companies to maximize ridership. That buys political legitimacy for the privatized system, which is necessary for the continued provision of capital expansion subsidies. Indeed, during the long deflation era between 1992 and 2022, it was common for operators to charge below the maximum, and the real value of railway fares continued to rise. Fare maximums are set on the basis of the average cost structures of all railway operators in a region, so companies with below-average costs like Tokyu would often charge below the cap to maintain a competitive edge, prevent public backlash, and maximize traffic to their side-businesses.

Other than the fare maximums, the railways are free to make their own decisions about timetables, service patterns and day-to-day operations, a highly specialized and technical task which requires deep expertise. This contrasts with the government meddling with, say, Amtrak’s routes.

Carefully designed public subsidies also play a useful role. Although Japanese railways do not receive subsidies for day-to-day operations, they do receive government loans and grants for capital investments. These are typically tied to public priorities, such as disability access or earthquake-proofing, or to projects that have large spillovers that the railway company would be unable to internalize, like removing level crossings, or elevating at-grade railways or trams in order to reduce road congestion and accident risk. Generally, the local prefectural government will match the contribution of the national government. Larger new build projects are subject to lease back or debt-payment conditions that fare revenue is expected to pay back.

The recipe for successful railways

Railway companies invested heavily in real estate businesses, often funding lines through selling land for housing around new stations. Liberal spatial policy meant that such development happened easily, even as it enabled dense development in urban cores where radial rail lines converged. Rail companies were generally vertically integrated regional monopolies, owning the land, track, and rolling stock, setting their own timetables, and employing their staff. The state imposed controls to stop them exploiting their monopoly position, but it did so cautiously, allowing them to make sufficient profit that incentives to invest were preserved. Capital subsidies were targeted at providing specific public goods that normal commercial operations overlooked.

The above paragraph could be written by a historian of the future about contemporary Japan. But every word in it could also be written by a historian today about the United States in the nineteenth century – usually seen as the epitome of capitalist individualism. This striking fact contradicts the idea that America’s supposed individualism foreordains it to be the land of the car, or that Japan’s supposed communitarianism foreordained it to be the land of rail.

It also puts pressure on the idea that the demise of rail is the inevitable consequence of cars. All countries saw some shift to cars in the twentieth century, and all rail industries had to respond to that. But public policy had an enormous effect on how successfully they did so. The rise of zoning restrictions on density, excessive price controls, nationalization, and vertically disintegrated privatization have hampered Western rail in remaining competitive against cars since the 1920s. By maintaining and restoring the institutions that built the first railway systems in the nineteenth century, the Japanese have created the mightiest railway system of the twenty-first.